The article explains the objectives and users of general purpose financial statements. This helps to determine what information are relevant to the users.

by THEACCSENSE April 16, 2021 Updated January 2, 2023

In our earlier publication Accounting 101: Introduction to Accounting, we understand that financial reports are the output of an accounting process. There are various types of financial reports and one of the financial reports commonly used by people is the financial statements.

What is a financial statement? Why are financial statements important? What is the information included in the financial statements? In this article, we bring readers to understand the objectives of financial statements and who are the users of the financial statements.

Financial statement is a financial report prepared by the management of an entity to tell the story about the financial position and performance of the entity at a certain financial reporting date or period. There are two types of financial statements prepared by a company:

A special purpose financial statement is prepared for a specific purpose(s) and for a limited group of recipients or users. This type of financial statement is prepared for example, for the board of directors of the company in a proposed merger and acquisition or for an initial offering. General purpose financial statements, on the other hand, are prepared for a broad range of users such as investors, lenders, or other creditors.

Companies prepare the general purpose financial statements as part of the requirements set by the oversight authorities to report on the financial affairs of the companies. Entities prepare financial statements based on the financial reporting framework appropriate for the company according to the jurisdiction where it operates.

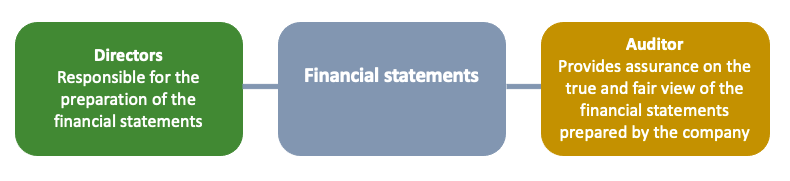

The responsibility for the preparation of the financial statements lies with the directors of the company. In Malaysia, Section 248 of the Companies Act 2016 clearly states that directors of every company have the responsibility to prepare financial statements of the company. Directors are liable to a fine of not exceeding RM500,000 or imprisonment of not exceeding one year or both if they failed to prepare the financial statements within the stipulated time frame.

Auditor, which is an independent party from the entity, provides assurance on the financial statements. Auditors provide assurance that the financial statements prepared by management reflect the true and fair view of the financial condition and performance of the company.

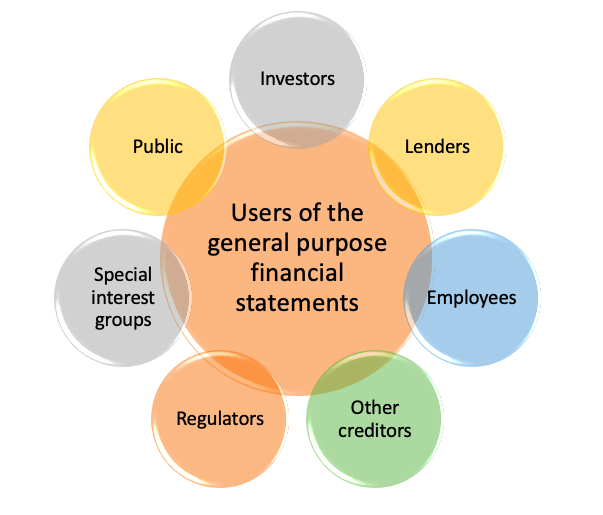

As explained earlier, entities prepare general purpose financial statements to provide financial information about the reporting entity for a broad range of users.

Who are the users of the general purpose financial statements? They are the group of users who are not able to obtain or demand financial information to be provided to them directly to meet their objective or intention.

It is impossible for standard-setters to consider all users in developing the financial reporting standards. This is because different users have different financial information needs. Accordingly, there is a specific group of users that standard-setters focused on in developing the financial reporting standards. This group of users is called “primary users”.

The primary users may also be different from one financial reporting framework to another. For instance, the Conceptual Framework for Financial Reporting issued by the MASB clearly states that the general purpose financial reports prepared under the MFRS framework are not primarily directed to other parties such as regulators and members of the public other than investors, lenders and other creditors.

Although regulators and members of the public may find the general purpose financial statements useful, the standard-setter may not necessarily consider the information needed by these users in the development of standards.

Unlike special purpose financial statements which are prepared to meet the specific purpose or information needed of the requestor, financial information provided in the general purpose financial statements may not provide all of the information that the primary users expect from the entity.

Nevertheless, the general purpose financial statements are prepared based on a financial reporting framework. The framework has considered the information needed of the primary users of the general purpose financial statements. The general purpose financial statements help to provide useful information to the primary users in making their economic decisions about providing resources to the entity. Additionally, it also helps users to assess the performance and accountability of the entity in utilising the resources provided to them.

| Financial reporting framework | Primary users of the general purpose financial statements | Objectives of the general purpose financial statements |

|---|---|---|

| Malaysian Financial Reporting Standards (“MFRS”) framework | Existing and potential investors, lenders and other creditors | To provide financial information about the reporting entity that is useful to the primary users in making decisions about providing resources to the entity |

| Malaysian Private Entities Reporting Standard (“MPERS”) framework | A broad range of users | To provide information about the financial position, performance and cash flows of the entity that is useful for economic decision-making by a broad range of users of the financial statements |

| International Public Sector Accounting Standards (“IPSASs”) framework | Service recipients and resource providers of the public sector entities | To disclose the information that the users (who do not possess the authority to require a public sector entity) need for accountability and decision-making purposes |

Financial reporting framework, primary users and objectives of the general purpose financial statements